How Crypto Yield Persists

Or, More Often, Does Not

Understanding where yield comes from is step one.

Understanding how/when it can persist is step two.

That’s what I’ll be discussing in this post.

Many naive, starry-eyed crypto participants (including me - back in the day) evaluate yield by looking at APY.

Some more savvy investors study protocol mechanics or source code.

But very few know to ask the most important question:

What has to stay true for this to keep working?

That question is the key difference between exposure that adapts with conditions vs. exposure that is sadly dependent on fragile mechanisms.

(You may have heard the Sunday school song about the wise man who built his house upon the rock and the foolish man who built his house upon the sand. If the metaphor fits…)

This post will identify three common conditions to watch for when trying to assess whether your DeFi yield will persist or falter. And how to recognize which of them you - and your money - are operating under.

The Three Conditions

Condition A: Demand-Funded Continuity

What it is

Yield persists as long as there is ongoing demand for the underlying service.

Structural characteristics

payment comes from users who require the service

yield does not depend on inflationary token emissions

continuation of yield does not require new participants

yield scales with usage rather than growth

When it persists

As long as the underlying activity continues to be valued by the market.

If people trade less, borrow less, or use the network less, yield declines proportionally.

The mechanism itself does not break simply because demand declines.

When it falters

When a system becomes obsolete, a network or protocol ceases to operate, or when alternatives emerge that cause material disruption.

Examples (illustrative structures, not endorsements)

validator staking rewards (persist for as long as the network operates and staking rewards are legal)

swap fees in active trading pairs (persist for as long as traders keep trading)

borrowing interest in lending protocols (persist for as long as borrowing demand exists)

Key insight

Demand-funded yield does not require infinite growth.

It does require continued use.

Condition B: Incentive-Driven Temporality

What it is

Yield persists as long as a protocol chooses and is economically able to effectively subsidize participation.

Structural characteristics

payment comes from inflationary token emissions or limited treasury assets

yield often depends on protocol-defined incentive schedules

continuation is a policy decision, not a metrics-driven outcome

yield magnitude can fluctuate independently of activity or usage levels

When it persists

As long as incentive programs remain active under current parameters.

When it falters

When emissions taper as scheduled, when incentive budgets are exhausted, or when governance removes subsidies.

Examples (illustrative structures, not endorsements)

liquidity mining programs paying for deposits in a separate token

bonus yields associated with staking derivatives

protocol launch incentives during bootstrap phases

Key insight

Incentive-driven yield is (most often) intentionally temporary.

It is designed to influence behavior to establish traction during a specific phase, not to function indefinitely.

The relevant questions do not revolve around whether subsidies are “sustainable,” but rather around how long the protocol intends to pay them, and the long-term tokenomics of what is paid out.

Condition C: Flow-Dependent Fragility

What it is

Yield persists only for as long as new participants continue depositing.

Structural characteristics

payment comes from new deposits rather than from service fees or protocol budgets

continuation depends on user-base growth rather than feature usage levels

mechanisms destabilize rapidly when new inflows slow or collapse

When it persists

Only for as long as new participants enter at a rate sufficient to fund payouts to existing participants.

When it falters

When new user deposits slow, when market conditions change, or when participant confidence declines.

Failure is often non-linear: the system can appear stable until conditions suddenly shift.

Examples (illustrative structures, not endorsements)

reflexive token models where prospective APY depends on price appreciation

yield structures tied directly to TVL (total value locked) growth

mechanisms where yield depends on expanding leverage parameters and liquidation activity

Key insight

Flow-dependent mechanisms require continuous expansion.

Because growth is finite, these structures are inherently fragile.

The relevant question is not whether the yield is currently working, but what happens when inflows stop.

Applying the Framework

Same Protocol, Different Conditions

Many protocols contain multiple yield components operating under different conditions.

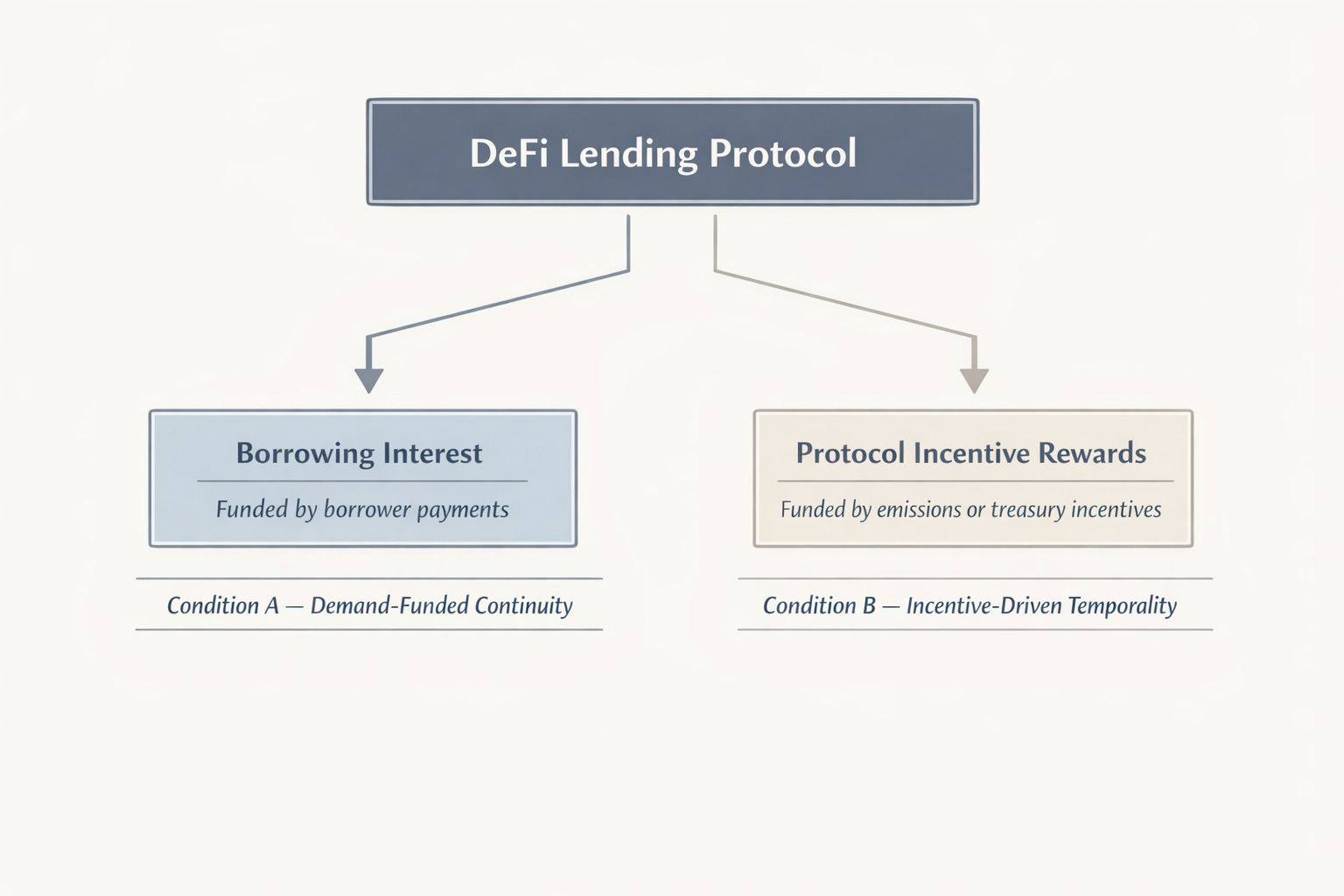

Example: a lending protocol (illustrative structure)

Borrowing interest — Condition A (demand-funded continuity)

Persists as long as borrowing demand exists.Protocol incentive rewards — Condition B (incentive-driven temporality)

Persist only while emissions or incentive programs remain active.

Separating these components allows persistence to be evaluated independently.

Same Mechanism, Different Contexts

The same mechanism can exhibit different persistence characteristics depending on context.

Example: liquidity provision (illustrative structure)

In an established, high-volume pool:

Swap fees reflect ongoing trading demand (Condition A).In a new or low-volume pool with incentives:

Most yield derives from emissions rather than fees (Condition B).

The action is the same.

The persistence profile is not.

Questions to Ask

When evaluating yield persistence, ask:

What funds the yield?

Service fees, protocol incentives, or participant inflows?What has to stay true for it to continue?

Continued usage, continued subsidies, or continued growth?What happens if conditions change?

Will yield decline gradually, or will the mechanism fail rapidly?What stops if incentives end?

Can temporary and durable yield be cleanly and logically separated?

If these questions cannot be answered, the persistence profile of the yield is not understood.

How This Framework Is Used

This framework does not predict outcomes.

It classifies persistence conditions.

It allows yield to be evaluated based on:

dependency structure

continuation requirements

observable failure modes

This enables clearer analysis without reliance on price forecasts or performance projections.

Final Thought

Crypto yield operates under one of three structural conditions:

Demand-funded continuity — persists with ongoing usage

Incentive-driven temporality — persists with active subsidies

Flow-dependent fragility — persists only with continued inflows of users and/or capital

Each behaves differently as conditions change.

Understanding which condition(s) govern a yield mechanism allows persistence to be evaluated explicitly. Not by headline APY, but by structural resilience.

Thank you for reading.

Unclear on something? Want a topic covered? Submit Your Questions Here

I read everything. Good questions may become future posts.

If this analysis was useful, Moondance Research goes deeper.

I publish one paid piece each week focused on structural risk, capital protection, and honest yield literacy.

Paid subscribers receive the full archive, reference-grade frameworks, and downloadable artifacts designed to spot opportunities and reduce the probability of getting financially wrecked.

Founding 100 subscribers receive permanent preferred pricing as recognition for supporting Moondance in its earliest phase.