Why Most Airdrop Hunters Lose Money

What the Screenshot Doesn't Show

There is always a screenshot.

Someone posts their wallet balance. Five figures, sometimes more. “Just for using the protocol.” The comments fill with questions about how to replicate this great success. The next round of activity begins.

What the screenshot fails to show is the pile of attempts that paid nothing. Gas fees. Bridging costs. Hours spent qualifying for eligibility criteria that turned out to be retroactive, opaque, or quietly sybil-filtered. Tokens that were claimed, held far too long, and sold for a pittance into a market that had already moved on.

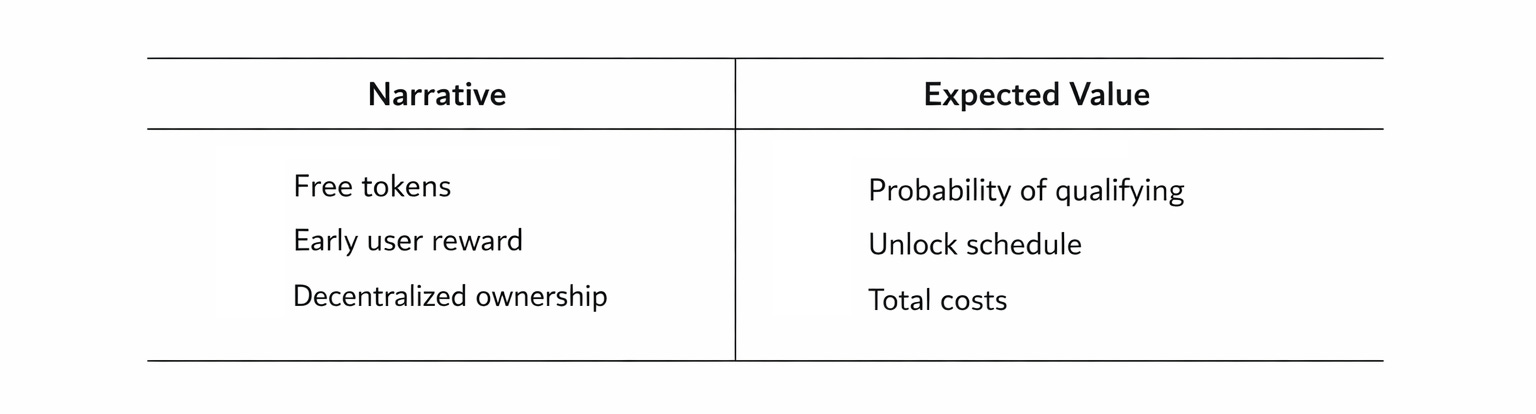

Airdrops are not gifts from benevolent protocols. They are marketing budgets, paid out in freshly minted tokens instead of dollars. It is calculated.

Airdrop chasing can be a rational activity for crypto holders, but most avid “hunters” approach them irrationally and get burned.

Defining “Airdrop”

Protocols distribute tokens to accomplish something specific: stimulate usage, seed governance participation, reward early adopters, and/or generate liquidity. The “payment” isn’t cash. It’s token supply, newly created, with a market price that exists strictly because someone else is willing to buy it.

Arbitrum’s airdrop in early 2023 is an example worth discussing. The protocol distributed 12.75% of overall total supply via their initial TGE (token generation event), split between users and DAOs.

Eligibility based on points/activity/ heuristics was announced retroactively. The unfortunate implication is simple. You could have been active for months and still received the minimum 625 tokens, or nothing at all, depending on behavior patterns that weren’t announced in advance.

That’s not a windfall. It’s an audition you didn’t know you were in. With a payout structure you had no way to predict in advance.

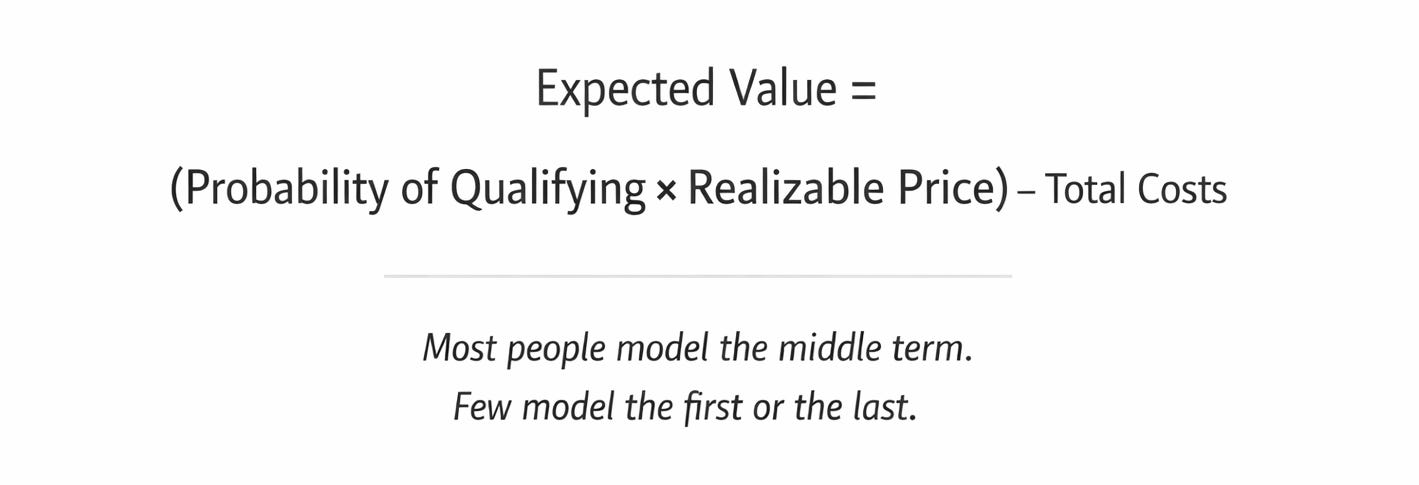

Expected Value

Expected value is not a complex concept. It is:

1) the probability of a good outcome,

2) times the value of that outcome,

3) minus costs.

Most airdrop analysis quietly skips the first and third parts entirely, focusing only on hope of “number go up.”

Probability of qualifying. Eligibility is not guaranteed. As in the case of Arbitrum’s airdrop, criteria are often retroactive. Sybil filters err on the side of disqualifying a large number of wallets, meaning interactions that “should” count sometimes do not.

Dirty industry secret: in competitive farming environments, the people who maximize allocation are usually the ones who somehow understood the evaluation model before it was public. Everyone else gets to guess and play catch up.

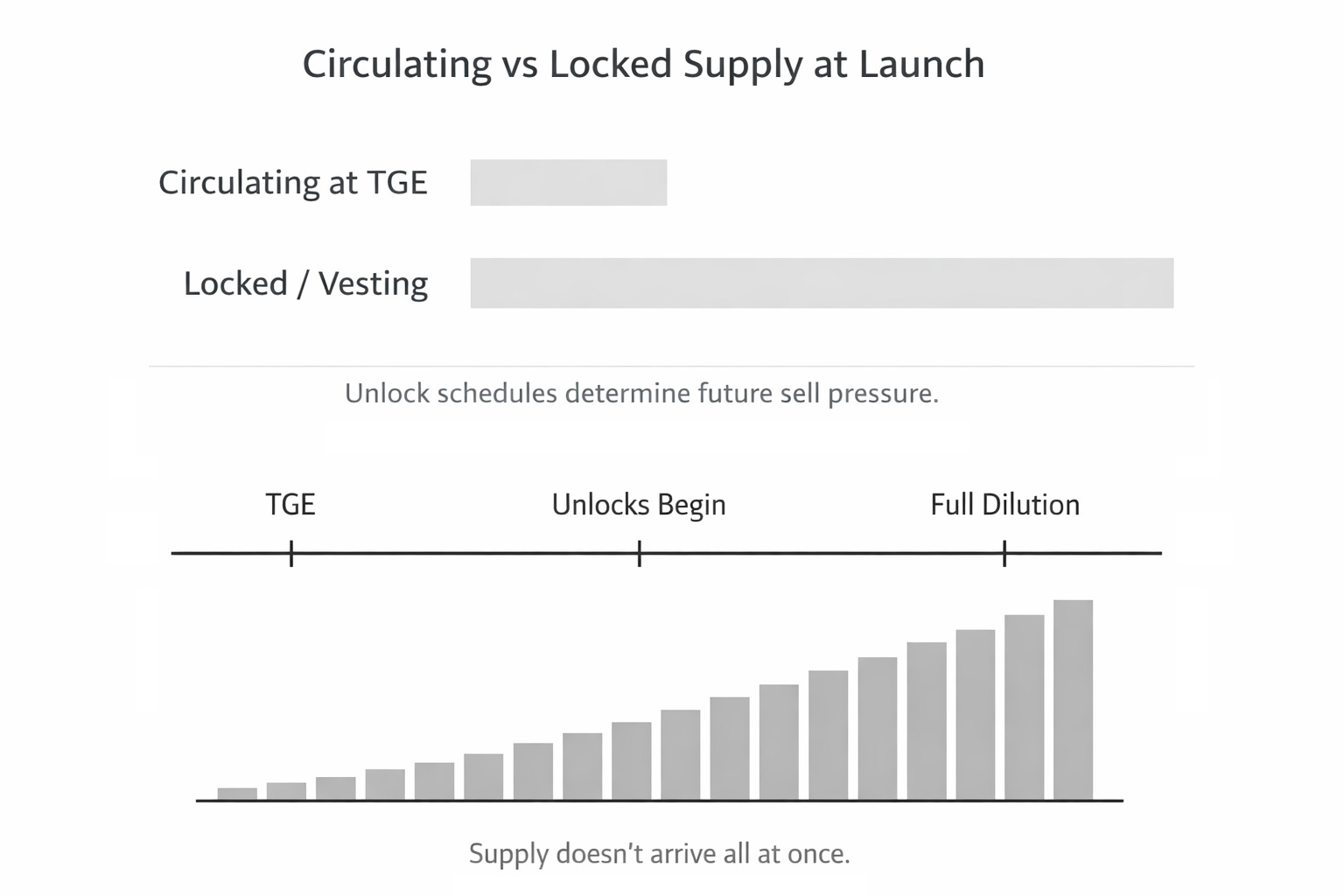

Value of the tokens you receive. Opening price is not realized price. It’s the first moment of price discovery, usually on thin liquidity, usually at peak attention. Supply coming online after that initial moment matters a lot. Not primarily from recipients selling, but from the unlock schedules.

Optimism’s token distribution illustrates this structure. Roughly 29 to 31% of OP supply is insider allocation, with multi-year vesting behind a relatively small initial float. The airdropped portion looked meaningful in isolation. Against total supply and the tokens still locked, it is simply not. When this pattern plays out, you see the fallout months later, as price weakens while supply keeps coming.

Costs. This is the least visible part of the calculation.

Transaction fees. Bridging costs. Slippage. Opportunity cost of capital tied up in protocols while you wait. Time spent monitoring, qualifying, executing. Smart contract risk of immature, unproven protocols. And the devastating hidden cost of holding tokens through a drawdown hoping for “number go back up.”

A few dollars per interaction on an Ethereum L2 adds up fast when repeated dozens of times. And most attempts don’t pay out. The winning screenshot is averaging across a lot of blank rows and zeroes that don’t get publicized.

Incentive Traps

There are three patterns worth naming.

Behavior rent. Protocols use token emissions to rent the behavior they need: trading volume, liquidity, governance participation. BLUR ran multiple seasons of airdrop emissions that drove massive NFT trading volume. Once emissions tapered and NFT volumes normalized, holders absorbed the resulting sell pressure and eventually paid for it. BLUR’s governance structure also included a 180-day freeze on fee switch voting after launch, which meant holders were prevented from enforcing mechanisms that might have boosted token value. The observable outcome: BLUR opened around $0.71 in early 2023 and was trading around $0.02 by early 2026.

Unlock shocks. Even if the initial airdrop was priced fairly, later supply arrivals can reset the price people are willing to pay. PYTH, the Pyth Network oracle token, experienced an unlock in May 2024 that increased circulating supply by approximately 105% in a single event. This unlock wasn’t hidden. It was in the tokenomics documentation the whole time. But it rarely appears in the screenshots that circulate when a token first launches. And it is simply not often properly researched and evaluated by hunters.

Distribution-day mechanics. When a large user base receives liquid inventory at once, many of them immediately sell. This is not irrational. It is the predictable outcome of distributing tokens to people whose primary interest was profiting from the tokens, not the protocol itself. Wormhole’s token fell approximately 24% within hours of its airdrop opening. It partially recovered. But the person who claimed at open and held through the initial drop did not experience the “free money” experience that many flashy screenshots imply.

These examples are common enough in the industry that they should change your default set of assumptions.

Re-evaluating

Certain conditions improve potential airdrop math: low interaction costs (i.e. per-transaction gas fees), explicit and stable eligibility criteria, transparent supply schedules with no large backloaded cliffs. And most importantly, a clear mental limit on how much time and capital you’re willing to commit before the outcome is known.

In other words: if interaction costs are near zero and supply is largely circulating at launch, the calculus changes.

Opposing conditions that destroy expected value are also readily observable: opaque and/or retroactive criteria, heavy insider allocations vesting after the TGE, repeated high transaction costs against uncertain claims, and the bad habit of treating opening price as a reference point when it is actually the most optimistic moment in the token’s life.

Final Thoughts

A calmer posture is to model an event before treating it as potential profit. If you haven’t estimated expected value, you’re not farming. You’re hoping at best, gambling at worst.

The bottom line: the math always looks better in a braggart’s screenshot than it does in a rational evaluation spreadsheet. Airdrops can be rational. Most airdrop hunting, as practiced, is not.

A note on what this post doesn’t claim

There is no standardized, peer-reviewed dataset showing exactly what percentage of major token launches trade below opening price at six months. That work requires computing from raw price and on-chain data, and the methodology varies enough that no clean public number exists. The examples above are real and sourced. They suggest a pattern. They do not prove a universal law.

That distinction matters. The goal here is to change your default assumptions, not to give you false precision to argue from.

Thank you for reading.

Unclear on something? Want a topic covered? Submit Your Questions Here

I read everything. Good questions may become future posts.

If this analysis was useful, Moondance Research goes deeper.

I publish one paid piece each week focused on structural risk, capital protection, and honest yield literacy.

Paid subscribers receive the full archive, reference-grade frameworks, and downloadable artifacts designed to spot opportunities and reduce the probability of getting financially wrecked.

Founding 100 subscribers receive permanent preferred pricing as recognition for supporting Moondance in its earliest phase.